Artificial Intelligence

Robotic Process Automation Market to Hit USD 23.9 Bn by 2030

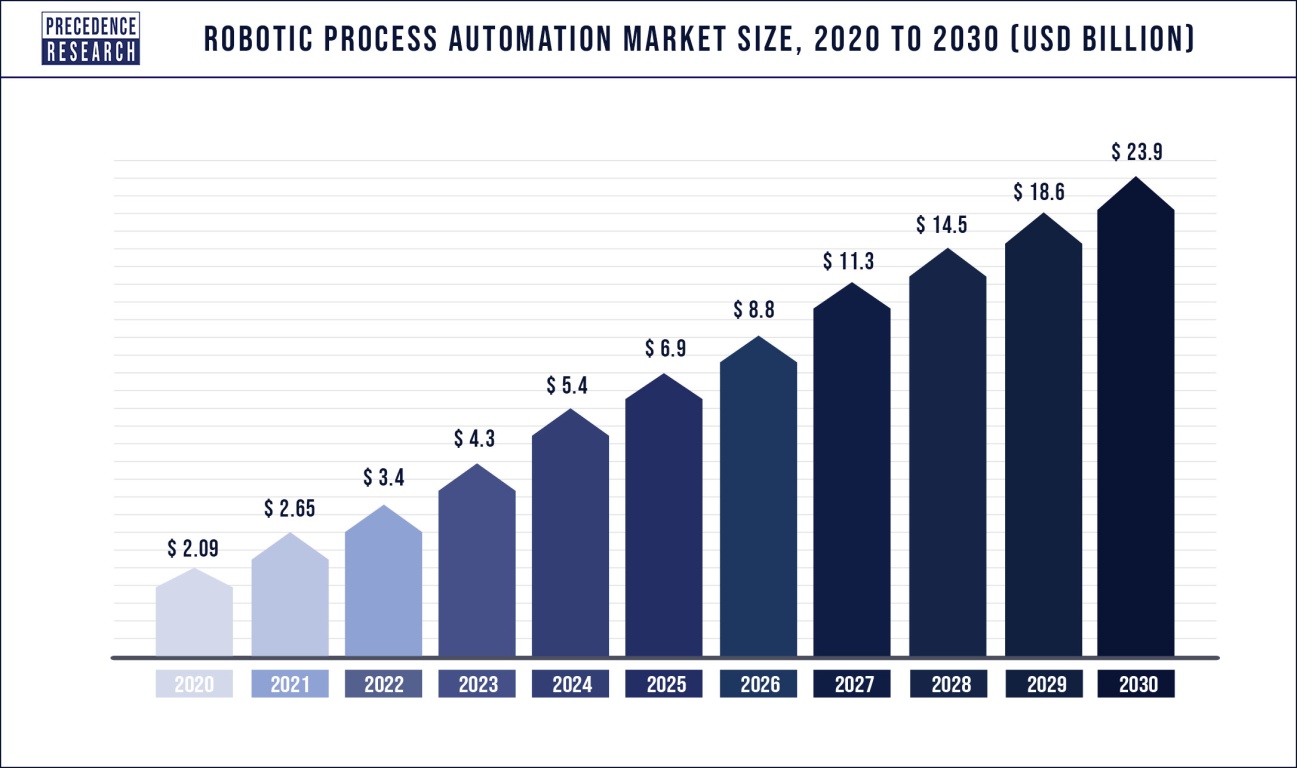

London, Jan. 06, 2022 (GLOBE NEWSWIRE) — According to Precedence Research, the global robotic process automation market size was valued at USD 2.65 billion in 2021. Robotic process automation (RPA), sometimes known as software robotics, employs automation technology to replicate back-office functions performed by human workers, such as data extraction, form completion, file movement, and so on. It integrates and performs repetitive operations between enterprise and productivity apps by combining APIs and user interface (UI) interactions. RPA technologies complete autonomous execution of diverse tasks and transactions across unconnected software systems by deploying scripts that replicate human operations.

Get the sample copy of report@ https://www.precedenceresearch.com/sample/1348

Crucial factors accountable for market growth are:

- Penetration of RPA to manage complicated unstructured data and automate any business operation

- Increasing Adoption of Artificial Intelligence and Cloud-Based Solutions

- High demand for RPA services from BFSI sector

- The innovation and technological advancement

- The increasing focus on reducing the burden of medical professionals

Scope of the Robotic Process Automation Market

| Report Coverage | Details |

| Market Size In 2021 | USD 2.65 Billion |

| Growth Rate From 2021 to 2030 | CAGR of 27.7% |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Base Year | 2021 |

| Forecast Period | 2021 to 2030 |

| Companies Covered | UiPath, Celaton Ltd., Automation Anywhere, Blue Prism, NICE, EdgeVerve Systems Ltd., Pegasytems, KOFAX, Inc., NTT Advanced Technology Corp., FPT Software, OnviSource, Inc., HelpSystems, Xerox Corporation |

Regional Snapshots

North America is the market’s most dominant region, while Asia Pacific is the fastest expanding in the RPA industry. The financial markets in the United States are the world’s largest and most liquid. Finance and insurance accounted for 7.4 percent (or $1.5 trillion) of US GDP in 2018. Leadership in this vast, fast-growing sector generates significant economic activity and direct and indirect job creation in the United States. Financial services and products aid in the facilitation and financing of the export of manufactured goods and agricultural products from the United States. The insurance industry’s net premiums written totaled $1.1 trillion in 2016.

According to NAIC data, premiums collected by life and health insurers accounted for roughly 53%, while premiums collected by property and liability insurers accounted for 47%. Furthermore, approximately one-third of all reinsurance sold globally is purchased by companies based in the United States. International insurance businesses are constantly seeking business agreements and collaborations with American insurers. The dominance of the BFSI industry in North America has a beneficial impact on the RPA market.

Ask here for customization study@ https://www.precedenceresearch.com/customization/1348

Report Highlights

- Based on the type, Service segment is the most dominating in the RPA market due to the rise in demand for outsourcing RPA and installing software over the cloud for automation.

- The on-premises segment is the major contributor in the RPA market due to its in-house ownership.

- The BFSI segment held the largest share in the RPA market. Based on the industry, the BFSI segment holds the largest market share. Banking and insurance businesses use RPA for regulatory reporting and balance sheet reconciliation.

Market Dynamics

Driver

Large enterprises will increase the capacity of their existing RPA portfolios by 2024. The majority of new spend will come from large enterprises purchasing new add-on capacity from their original vendor or ecosystem partners. Organizations will need to add licenses to run RPA software on new servers as they grow, as well as additional cores to handle the strain. This tendency is a logical reflection of the increasing demands on an organization’s “everywhere” infrastructure. RPA use will expand as corporate users become more aware of its benefits.

In fact, Gartner projects that by 2024, over half of all new RPA clients would come from business buyers outside of the IT group. In the near future, such factors will drive the robotic process automation industry.The stats for KYC alone are staggering. In 2017, financial institutions spent USD 150 million on KYC procedures, with expenses likely to rise by 13% over the next year. Similarly, onboarding new clients now takes 26 days, up from 24 days in 2016, and firms predict a 12% increase by the end of 2018. According to industry analysts, RPA can assist merging banks in easing compliance processes that require heavy lifting from banks. The increased demand in the BFSI industry would drive the RPA market throughout the forecast period.

Restraint

RPA Infrastructure and Customization Issues Will Restrain Market Growth

A corporation must have sufficient infrastructure and a professional team to oversee all operations before installing an RPA technology. It is tough, complex, and expensive to set up infrastructure, hire professionals, train existing personnel, and install thousands of bots. The platform on which RPA bots operate changes frequently, and the requisite adaptability isn’t always included into the bots. As a result, many firms resist implementing RPA in their operations.

Opportunities

The rising trend of cloud-based solutions and the increased usage of robot-based solutions

As enterprises pursue new IT architectures and operational philosophies, they lay the groundwork for new digital business prospects, including next-generation IT solutions. Organizations that embrace dynamic, cloud-based operational models will be more competitive, particularly in today’s fast changing business climate. These firms appreciate not only the short-term benefits of cloud computing, but also position themselves to be early adopters of disruptive developments that will shape the future.

Cloud services are rapidly being used by organizations for new initiatives or to replace current systems, implying that investment on traditional IT solutions is shifting to the cloud. According to the most recent Gartner IT spending report, investment on data center systems is expected to be USD 188 billion in 2020, a 10% reduction from 2019. By 2024, traditional solutions will account for more than 45 percent of IT spending on system infrastructure, infrastructure software, application software, and business process outsourcing.Because of this growth, cloud computing has been one of the most persistently disruptive forces in IT industry since the dawn of the digital age. This creates an opportunity for the RPA market players.

Challenges

Organizational culture

While RPA will diminish the need for certain employment categories, it will also encourage the creation of new roles to handle more complicated tasks, allowing employees to focus on higher-level planning and creative problem-solving. As responsibilities within job positions alter, organizations will need to foster a culture of learning and innovation. The adaptability of a workforce will be critical to the success of automation and digital transformation programs. Employees may prepare teams for ongoing shifts in objectives by educating personnel and investing in training programs.

Related Reports

Recent Developments

- In October 2019 Automation Anywhere, a global RPA vendor, said that it would extend operations into the Greater China Region (GCR) by building multiple regional offices.

- In February 2019,Datamatics collaborated with Mumbai Metro to secure an automated fare collection contract for Metro Lines 2A, 2B, and 7.

- For instance, in March 2021, UiPath bought Cloud Element, an API integration platform startup.

- In March 2021, Automation Anywhere collaborated with Google to help build a new portfolio of technologies that can automate basic job responsibilities in organizations.

Segments Covered in the Report

By Type

- Software

- Service

- Consulting

- Implementing

- Training

By Deployment

- Cloud

- On-Premise

By Industry

- BFSI

- Pharma & Healthcare

- Retail & Consumer Goods

- Information Technology (IT) & Telecom

- Communication and Media & Education

- Manufacturing

- Logistics, and Energy & Utilities

- Others

By Geography

- North America

- U.S.

- Canada

- Europe

- U.K.

- Germany

- France

- Asia Pacific

- China

- India

- Japan

- South Korea

- Rest of the World

Click Here to View Full Report Table of Contents

Buy this Premium Research Report@ https://www.precedenceresearch.com/checkout/1348

You can place an order or ask any questions, please feel free to contact at [email protected] | +1 9197 992 333

About Us

Precedence Research is a worldwide market research and consulting organization. We give unmatched nature of offering to our customers present all around the globe across industry verticals. Precedence Research has expertise in giving deep-dive market insight along with market intelligence to our customers spread crosswise over various undertakings. We are obliged to serve our different client base present over the enterprises of medicinal services, healthcare, innovation, next-gen technologies, semi-conductors, chemicals, automotive, and aerospace & defense, among different ventures present globally.

For Latest Update Follow Us:

https://www.linkedin.com/company/precedence-research/

https://www.facebook.com/precedenceresearch/

https://twitter.com/Precedence_R

Artificial Intelligence

Clinical Trials Matching Software Market Projected to Reach $832.56 million by 2030 – Exclusive Report by 360iResearch

PUNE, India, April 18, 2024 /PRNewswire/ — The report titled “Clinical Trials Matching Software Market by Functionality (Analytics & Reporting, Compliance Tracking, Data Management), Deployment (Cloud & Web Based, On-Premise), End-Use – Global Forecast 2024-2030” is now available on 360iResearch.com’s offering, presents an analysis indicating that the market projected to grow from a size of $342.20 million in 2023 to reach $832.56 million by 2030, at a CAGR of 13.54% over the forecast period.

“The Global Surge in Adoption of Matching Software for Enhanced Participant Enrollment”

Clinical trials matching software stands at the forefront of revolutionizing clinical research by automating the process of identifying and enrolling eligible participants. These platforms offer a streamlined approach to match patient health profiles with trial requirements, accelerating enrollment and supporting the shift toward personalized healthcare using these advanced AI and ML technologies. Although integrating these systems poses challenges due to variations in healthcare IT infrastructure and the imperative for rigorous data security, the potential for market growth is substantial. In the Americas, a robust clinical trials ecosystem thrives; in the European Union, it has unified regulatory standards and extended to emerging regions such as the Middle East, Africa, and the APAC countries; the demand for such innovative solutions is on a steep rise. This demand is fueled by governmental support, the evolving regulatory landscape, and strategic partnerships to embed these solutions within electronic health records, underscoring a global movement toward optimizing clinical trial processes to better cater to specific patient demographics.

Download Sample Report @ https://www.360iresearch.com/library/intelligence/clinical-trials-matching-software

“The Rise of Virtual Trials and Advanced Matching Software”

The healthcare landscape is witnessing a transformative shift toward virtual clinical trials, fueled by technological advancements and the necessity for continuity during the COVID-19 pandemic. This transition supports research amid social distancing measures and introduces significant cost savings by reducing the need for physical infrastructure and in-person interactions. The efficiencies brought by electronic health records (EHR), wearable technologies, and automation streamline the entire process, from patient recruitment to data analysis. Several approaches, endorsed by regulatory bodies such as the FDA, represent a leap forward in making clinical trials more accessible and streamlined, ensuring that more patients can participate in potentially life-saving research without the geographical and logistic constraints of traditional trials.

“Enhancing Clinical Trials through Advanced Analytics, Rigorous Compliance, and Precision-Patient Matching”

Integrating advanced analytics, meticulous compliance monitoring, and precision-patient matching marks a significant advancement toward maximizing efficiency and fostering trial diversity. The software delivers insightful data on trial progress, participant demographics, and enrollment figures, empowering stakeholders to make well-informed decisions and optimize resource distribution to meet trial goals effectively by implementing cutting-edge analytics. The built-in compliance feature ensures trials are conducted in strict adherence to regulatory standards, minimizing risks associated with non-compliance. Furthermore, a robust data management system guarantees the integrity and availability of clinical trial data, which is critical for the seamless operation and real-time analysis of trials. The software includes state-of-the-art patient matching technology, which employs sophisticated algorithms and artificial intelligence to expedite recruitment by accurately identifying candidates who match specific trial requirements. This innovative approach accelerates the recruitment timeline and enhances the diversification of trial participants, paving the way for more inclusive and representative clinical research outcomes.

Request Analyst Support @ https://www.360iresearch.com/library/intelligence/clinical-trials-matching-software

“Medidata by Dassault Systèmes SE at the Forefront of Clinical Trials Matching Software Market with a Strong 11.30% Market Share”

The key players in the Clinical Trials Matching Software Market include International Business Machines Corporation, Science 37, Inc. by eMed, LLC, Medidata by Dassault Systèmes SE, AutoCruitment LLC, Deep 6 AI Inc., and others. These prominent players focus on strategies such as expansions, acquisitions, joint ventures, and developing new products to strengthen their market positions.

“Introducing ThinkMi: Revolutionizing Market Intelligence with AI-Powered Insights for the Clinical Trials Matching Software Market”

We proudly unveil ThinkMi, a cutting-edge AI product designed to transform how businesses interact with the Clinical Trials Matching Software Market. ThinkMi stands out as your premier market intelligence partner, delivering unparalleled insights with the power of artificial intelligence. Whether deciphering market trends or offering actionable intelligence, ThinkMi is engineered to provide precise, relevant answers to your most critical business questions. This revolutionary tool is more than just an information source; it’s a strategic asset that empowers your decision-making with up-to-the-minute data, ensuring you stay ahead in the fiercely competitive Clinical Trials Matching Software Market. Embrace the future of market analysis with ThinkMi, where informed decisions lead to remarkable growth.

Ask Question to ThinkMi @ https://app.360iresearch.com/library/intelligence/clinical-trials-matching-software

“Dive into the Clinical Trials Matching Software Market Landscape: Explore 190 Pages of Insights, 286 Tables, and 22 Figures”

PrefaceResearch MethodologyExecutive SummaryMarket OverviewMarket InsightsClinical Trials Matching Software Market, by FunctionalityClinical Trials Matching Software Market, by DeploymentClinical Trials Matching Software Market, by End-UseAmericas Clinical Trials Matching Software MarketAsia-Pacific Clinical Trials Matching Software MarketEurope, Middle East & Africa Clinical Trials Matching Software MarketCompetitive LandscapeCompetitive PortfolioInquire Before Buying @ https://www.360iresearch.com/library/intelligence/clinical-trials-matching-software

Related Reports:

Clinical Trial Support Services Market – Global Forecast 2024-2030Virtual Clinical Trials Market – Global Forecast 2024-2030Clinical Trials Management System Market – Global Forecast 2024-2030About 360iResearch

Founded in 2017, 360iResearch is a market research and business consulting company headquartered in India, with clients and focus markets spanning the globe.

We are a dynamic, nimble company that believes in carving ambitious, purposeful goals and achieving them with the backing of our greatest asset — our people.

Quick on our feet, we have our ear to the ground when it comes to market intelligence and volatility. Our market intelligence is diligent, real-time and tailored to your needs, and arms you with all the insight that empowers strategic decision-making.

Our clientele encompasses about 80% of the Fortune Global 500, and leading consulting and research companies and academic institutions that rely on our expertise in compiling data in niche markets. Our meta-insights are intelligent, impactful and infinite, and translate into actionable data that support your quest for enhanced profitability, tapping into niche markets, and exploring new revenue opportunities.

Contact 360iResearchMr. Ketan Rohom360iResearch Private Limited,Office No. 519, Nyati Empress,Opposite Phoenix Market City,Vimannagar, Pune, Maharashtra,India – 411014.Email: [email protected]: +1-530-264-8485India: +91-922-607-7550

To learn more, visit 360iresearch.com or follow us on LinkedIn, Twitter, and Facebook.

Logo – https://mma.prnewswire.com/media/2359256/360iResearch_Logo.jpg

View original content:https://www.prnewswire.co.uk/news-releases/clinical-trials-matching-software-market-projected-to-reach-832-56-million-by-2030—exclusive-report-by-360iresearch-302119709.html

BOSTON, April 18, 2024 /PRNewswire/ — The RepTrak™ Company, the world’s leading reputation data and insights company, released its annual Global RepTrak 100 report. Utilizing its advanced reputation monitoring software, RepTrak gathered data from more than 243,000 survey responses across 14 major economies to rank the world’s 100 most reputable companies. They share that ranking alongside a full analysis of global corporate reputation trends and corresponding public sentiment in the 2024 report.

After two years of consecutive Reputation Score declines, this year’s Score is back up with an increase from 73.2 in 2023 to 73.8 in 2024. It’s a small increase after 2023’s full one-point drop. However, it’s an encouraging sign that companies have begun to recover from reputation falls driven by many challenges: macroeconomic issues, workplace difficulties, product problems, and corporate responsibility skepticism.

“This year’s report underscores a pivotal shift in the corporate landscape, spotlighting the remarkable adaptability and dedication of the Top 100 companies in responding to the dynamic needs of stakeholders,” states RepTrak CEO Mark Sonders. “The companies featured in our report are not just riding the wave of change; they are the ones steering it, proving that the best approach to business is one that embraces evolution and champions progress.”

RepTrak’s report explores how people thought, felt, and acted toward companies over the past year. Findings include notable increases in Conduct and Citizenship efforts, stakeholders’ rising willingness to invest, culturally resonant brand communications, and ESG Scores that soared despite skepticism around the acronym.

To read the full 2024 Global RepTrak 100 report, please visit: www.reptrak.com/globalreptrak

About RepTrak

The RepTrak™ Company is the world’s leading reputation data and insights company. We help companies by organizing and grading a variety of reputational elements, offering a real-world report card on their corporate reputation. Subscribers to the RepTrak program use our predictive insights to protect business value, improve return on investment, and increase their positive impact on society. RepTrak’s pairing of advanced metrics and dedicated reputation advisors offers clients an actionable analysis of their reputation data, aligning business objectives with stakeholder sentiment across different markets and sectors.

Established in 2004, The RepTrak Company owns the world’s largest reputation benchmarking database, gathering over 1 million company ratings per year used by CEOs, boards, and executives in more than 60 countries worldwide. For more information, please visit: www.reptrak.com

Logo – https://mma.prnewswire.com/media/2391550/RepTrak_Logo_Logo.jpg

Photo – https://mma.prnewswire.com/media/2391551/2024_GRT_Spreads__Instagram_Post.jpg

View original content:https://www.prnewswire.co.uk/news-releases/reptrak-announces-2024-global-reptrak-100-report-302121513.html

Artificial Intelligence

Group-IB takes part in a global operation to cripple Canadian Phishing-as-a-Service provider LabHost

SINGAPORE, April 18, 2024 /PRNewswire/ — Group-IB, a leading cybersecurity company aimed at investigating, preventing, and fight digital crime announced today that it participated in a coordinated global takedown operation against prominent Canadian Phishing-as-a-Service (PhaaS) provider LabHost, which has led to the arrest of 37 suspects across the United Kingdom and around the world by law enforcement agencies. As part of the operation, Group-IB also conducted an extensive analysis of LabHost’s criminal history and infrastructure, including insights into LabHost’s administrative platform and the services it provides to its purported user base which exceeds 2,000 subscribers worldwide, who illegally obtained around 480,000 card numbers, 64,000 pin numbers, and over 1 million passwords from victims used for websites and other online services, according to law enforcement agencies.

“By leveraging our Threat Intelligence and Digital Risk Protection, we are able to identify and monitor phishing attacks and websites like those deployed by LabHost and its subscribers around the world, enabling us to actively alert and protect our customers, and in turn, their customers as well,” said Dmitry Volkov, Chief Executive Officer of Group-IB. “Today’s takedown operation demonstrates the agility and responsiveness of our decentralized Digital Crime Resistance Centers, and how quickly we can provide immediate and local assistance wherever our customers may be.”

First uncovered in late 2021, LabHost emerged as a fully automated Phishing-as-a-Service (PhaaS) platform, streamlining the creation of phishing websites meticulously mirroring the interface and functionality of prominent banking, postal, and financial entities, aimed at intercepting, seizing, and profiting from users’ personal, credit card, and online banking credentials. Users are prompted to select from various “membership plans,” tailored to target businesses and individuals in either the United States and Canada, or globally, akin to mobile subscription models. These plans encompass “standard,” “premium,” and “world membership” tiers, priced between US$179 and US$300 monthly, with options for monthly, quarterly, or annual billing cycles.

For media inquiries, please contact [email protected]

Photo – https://mma.prnewswire.com/media/2391017/Group_IB.jpgPhoto – https://mma.prnewswire.com/media/2391018/Group_IB_2.jpgLogo – https://mma.prnewswire.com/media/1853638/4657466/Group_IB_Logo.jpg

View original content:https://www.prnewswire.co.uk/news-releases/group-ib-takes-part-in-a-global-operation-to-cripple-canadian-phishing-as-a-service-provider-labhost-302121388.html

-

Uncategorized7 days ago

Uncategorized7 days agoArm CEO Rene Haas will be delivering a Partner’s Event Speech at COMPUTEX 2024

-

Artificial Intelligence6 days ago

Artificial Intelligence6 days agoIn-Depth Analysis of Germany and France Data Center Markets: Germany Poised to Contribute Over $12.24 Billion Opportunities in the Next 6 Years – Arizton

-

Uncategorized7 days ago

BJEI: A New Record of High Performance in 2023 and a New Pattern of Diversified and Coordinated Development

-

Uncategorized7 days ago

Integrity Food Marketing Joins Forces with CA Ferolie to Expand East Coast Reach from Maine to Florida

-

Uncategorized7 days ago

Dimethyl Carbonate Market worth $1.9 billion by 2028 – Exclusive Report by MarketsandMarkets™

-

Artificial Intelligence6 days ago

Artificial Intelligence6 days agoCogX Festival Set to Debut in Los Angeles at Century Plaza on May 7th, 2024

-

Artificial Intelligence7 days ago

aelf Leads the Fusion of AI and Blockchain to Shape the Future of Technology

-

Artificial Intelligence7 days ago

Artificial Intelligence7 days agoXinhua Silk Road: Zoomlion Access pursues high-quality development with aerial work machinery sector innovation